2 DAY MEGA STOREWIDE SALE- TUESDAY & WEDNESDAY!

BUY LOCAL LOVE YOUR HOME SALE ENDS SATURDAY, MAY 9 AT 5PM!

FREE KWIK TRIP GAS CARD WITH PURCHASES OVER $1299*!

NO CREDIT CARD FEES!

1000'S of items IN-STOCK + 500 Mattresses

Largest Selection of USA Made + Amish Made Furniture & Mattresses

36 FLIP-ABLE Mattress Models!

2 DAY MEGA STOREWIDE SALE- TUESDAY & WEDNESDAY!

BUY LOCAL LOVE YOUR HOME SALE ENDS SATURDAY, MAY 9 AT 5PM!

FREE KWIK TRIP GAS CARD WITH PURCHASES OVER $1299*!

NO CREDIT CARD FEES!

1000'S of items IN-STOCK + 500 Mattresses

Largest Selection of USA Made + Amish Made Furniture & Mattresses

36 FLIP-ABLE Mattress Models!

Tuesday-Thursday 10am to 6pm | Friday 10am to 7pm | Saturday 10am to 5pm | Sunday Closed To Be With Family & Friends | Monday Showroom Closed

5430 West Layton Ave, Greenfield - Metro Milwaukee

You finally find the dining set that fits your room, or the sectional that feels right for movie night, and then your brain goes straight to the price tag. That’s normal. Furniture is one of those purchases that affects your everyday life, but it can still feel big and a little intimidating when it’s time to pay for it.

Around our store, we’ve had this conversation with Milwaukee families for generations. Since 1928, we’ve watched young couples furnish first apartments, parents replace worn-out sofas, and grandparents shop for a guest room that suddenly matters a lot more. Our customers don’t need a sales pitch. They need someone to explain the options plainly.

That’s what this guide is for.

Welcome to the Family Guide on Furniture Financing

A lot of folks walk into a furniture store excited, then get tense when the conversation turns to financing. They worry they’ll be pushed into something confusing, or that “easy” means “too good to be true.” We get it.

We’re a fourth-generation family business, and we’ve learned that financing only feels stressful when nobody slows down and explains it in plain English. If your sofa gave out, your mattress is past its prime, or your dining room is still waiting for real furniture, financing can be a practical way to bring home what your family needs without draining every dollar in savings.

That doesn’t mean every financing offer is a smart one. Some are simple and fair. Some come with catches. The key is knowing which is which before you sign anything.

A common real-life moment

Maybe you’ve just measured your living room and found a sectional that fits. Maybe you’re furnishing a condo, helping a parent move into senior living, or trying to replace a hand-me-down bedroom set with something built to last. In each case, the question isn’t only, “Can I afford this today?”

It’s also, “What’s the right way to pay for this so I still feel good about it later?”

Good financing should make your home more comfortable, not your budget more stressful.

We’ll keep this simple. We’ll talk through 0% promotions, store cards, personal loans, and buy now pay later plans. We’ll also highlight the traps, especially lease-to-own programs that look easy up front and cost far more in the long run.

Why Smart Financing Is Your Friend for Quality Furniture

Some people hear the word “financing” and think “debt.” Sometimes that’s fair. But sometimes financing is a tool. Used well, it helps you bring home furniture that serves your family now, instead of settling for something cheap that wears out fast.

Furniture isn’t just décor. It’s where your kids sprawl out after school, where guests sleep, where your back either gets support or doesn’t. If you buy a better-made sofa, solid wood dining set, or supportive mattress, you’re often buying fewer headaches later.

Buying once can be cheaper than buying twice

A bargain piece that sags, wobbles, or peels too soon isn’t really a bargain. Many families learn that the hard way. They save money in the moment, then replace the same kind of item again much sooner than planned.

That’s why easy furniture financing can be helpful when it’s attached to durable pieces. It gives you a path to choose something sturdier now, rather than “making do” and paying again later.

For larger furniture purchases, installment loans commonly split the cost into fixed payments over 12 to 24 months, and retailers may offer 0% APR promotions for 18 to 24 months on qualifying purchases, according to this furniture financing guide from STORIS. That kind of structure can make a solid-wood bedroom set or well-built sectional much easier to fit into a monthly budget.

Why local guidance matters

Online checkout buttons make financing look effortless, but they often don’t explain much. In a showroom, you can ask real questions.

What happens after the promotion ends if there is one?

Is the payment fixed or can it change?

Can this option work for a custom piece or a larger room package?

Does it make sense for this type of purchase or is there a better route?

That human piece matters. Financing should match the furniture and your household budget, not just get you approved fast.

If you want a little help making the whole purchase more manageable, our tips on how to shop for furniture smartly can help you think through quality, timing, and value before you commit.

Practical rule: If financing helps you buy better quality that you’ll use for years, it can be a smart move. If it pressures you into more than you can comfortably pay, it isn’t.

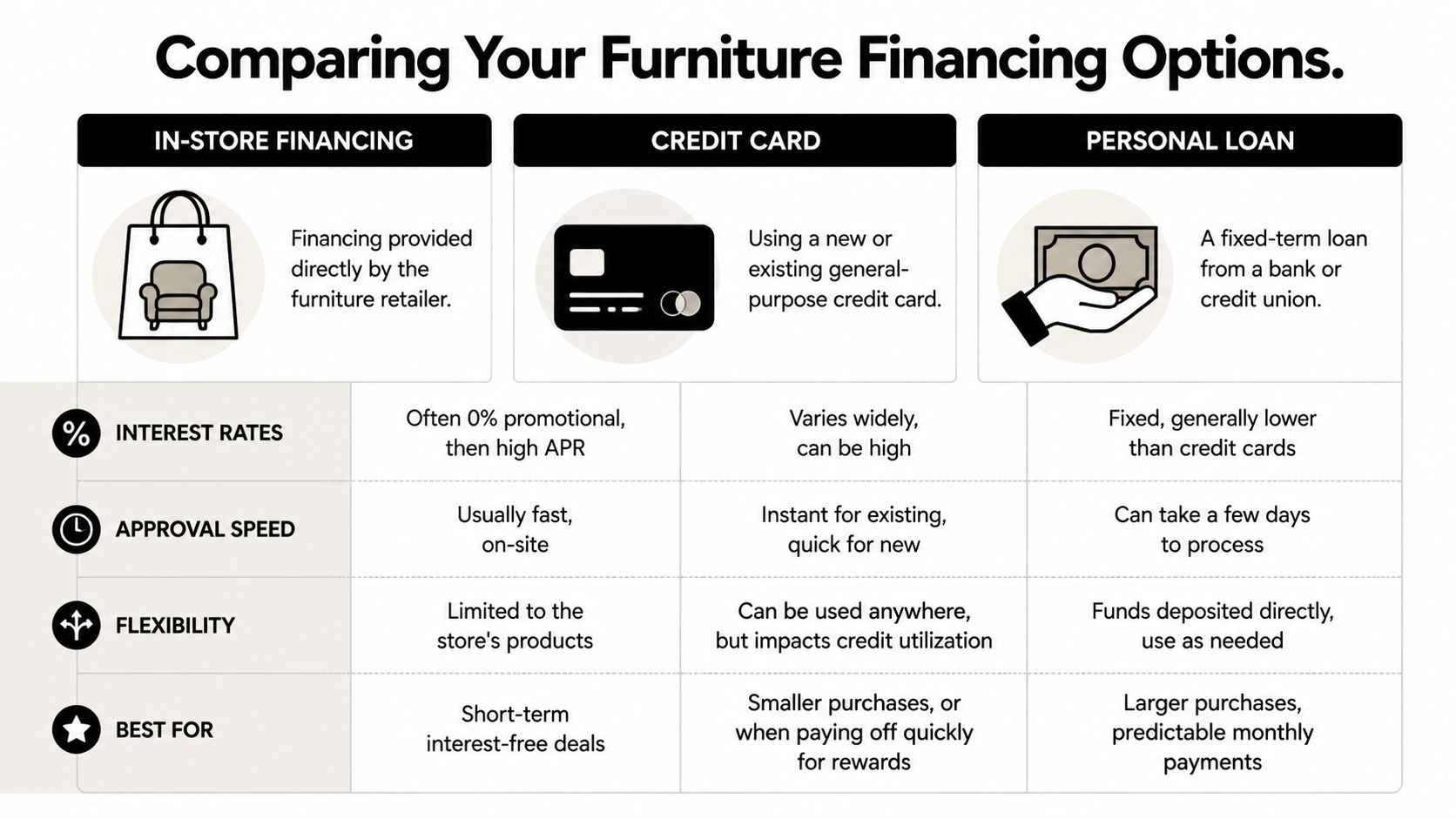

The Main Flavors of Furniture Financing Explained

Furniture financing gets confusing because several options can sound similar at checkout, even when they work very differently. Let’s sort them into plain, everyday language.

One reason this matters more now is that buy now, pay later lending grew sharply, with U.S. loan originations by five major lenders rising by 970 percent from 2020 to 2021, as shown in the CFPB report on BNPL market trends. So if it feels like these options are suddenly everywhere, you’re not imagining it.

In-store financing

This is often the most furniture-specific option. You choose the piece, fill out an application through the store or a financing partner, and if approved, you pay over time.

For many shoppers, this feels the most straightforward because the financing is tied directly to the purchase you’re making. It can also be a good fit for room packages, mattresses, recliners, dining sets, and custom orders that don’t line up neatly with a general-purpose credit card.

Think of in-store financing like sitting down with someone who understands both the product and the payment plan. You’re not just asking, “Can I get approved?” You’re also asking, “Does this plan make sense for this sofa, bed, or dining set?”

Store-branded credit cards

A store card is still a credit card, but it’s usually connected to one retailer or financing network. These often promote special financing windows, including no-interest offers for qualifying purchases.

This option can work well if you’re disciplined, understand the terms, and plan to pay within the promotional period. It can also be handy if you’re buying multiple items in one visit and want one account for the purchase.

Where people get tripped up is assuming “special financing” always means the same thing. It doesn’t. You need to ask how interest is handled, what happens if the balance remains after the promo period, and whether minimum purchase requirements apply.

Buy now pay later

BNPL is the quick, mobile-friendly option many people see online and in stores. In simple terms, it often breaks a purchase into smaller payments over a shorter period.

For smaller furniture-related expenses, BNPL can be convenient. Think accessory items, a mattress protector, delivery add-ons, or a modest purchase that you know you can finish paying off quickly. It may also appeal to shoppers who want a fast decision process.

Still, short repayment windows can be tight. Missing payments can lead to extra costs, so BNPL is easiest when the purchase amount is modest and your budget is steady.

Personal loans

A personal loan usually comes from a bank, credit union, or online lender. You borrow a set amount, receive the funds, and repay it in fixed monthly installments.

This can be useful when you want a clear term, one monthly payment, and flexibility to use the funds for more than one home purchase. Maybe you’re furnishing two rooms, or combining furniture with another household expense.

Here’s a simple way to understand:

In-store financing fits the furniture purchase itself

Store cards can be useful for promo offers

BNPL is often easiest for smaller, shorter-term buys

Personal loans can offer a broader, fixed-payment path

If you’re shopping for more than one room at a time, our ideas on furniture bundle deals can help you think through purchases in a more organized way before choosing a payment option.

Comparing Your Financing Options Side by Side

Reading about financing types is one thing. Comparing them at a glance is usually what helps people decide.

A useful starting point is this: consumer financing for furniture can range from 6.25% APR to 36% APR, and some store cards offer zero-interest financing for up to 24 months on purchases of $2,999 or more, while those offers often require a FICO score of 620 or higher, according to Credible’s overview of furniture loans.

Furniture financing options at a glance

Financing Type

Typical APR

Best For

BILTRITE Notes

In-store financing

Varies by program and approval

Larger furniture purchases, room packages, shoppers who want help understanding terms

Useful when you want to discuss the product and payment plan together in person

Store credit card

Can include promotional zero-interest offers, then may shift higher after promo terms

Shoppers with solid credit who can stay on top of promotional deadlines

Important to ask how interest works and what happens after the offer window

BNPL

Terms vary by provider, often designed for shorter repayment periods

Smaller purchases and add-ons you can pay off quickly

Good for convenience, less ideal when the monthly budget is already tight

Personal loan

6.25% APR to 36% APR

Larger purchases where fixed monthly payments matter most

Can be simpler for buyers who want funds not tied to one store account

Matching the option to the purchase

The financing type should fit the item, not just the approval screen.

For a mattress or recliner you may want predictable payments and simple terms.

For a whole room a store financing plan or personal loan may be easier to manage than several smaller payment plans.

For a smaller add-on BNPL can be practical if you know the short schedule won’t pinch your budget.

For buyers with stronger credit a promotional store card can be attractive, but only if you understand every deadline and condition.

The easiest option at checkout isn’t always the easiest option over the life of the purchase.

If credit concerns are part of your decision, our article on mattress financing with bad credit may help you think through the approval side with a little less stress.

Financing Pitfalls and How to Avoid Them

This is the part many stores skim over. We won’t.

Easy furniture financing should make life simpler. But some offers look easy only because the hard parts are tucked into the fine print.

Deferred interest can surprise people

A promotional offer can sound wonderful when you hear “no interest” or “special financing.” Sometimes it is a very good deal. Sometimes it’s a deferred-interest setup, which is different from a plain no-interest loan.

That difference matters. If a plan says you must pay the full balance within the promotional window, and you don’t, the leftover balance may not be the only problem. The interest treatment can be much harsher than people expected.

Before signing, ask these questions out loud:

Is this true 0% interest or deferred interest

What happens if I still owe even a small balance at the end

What is the APR after the promotional period

Is there a penalty for paying late

If the answers aren’t clear, slow down.

Lease-to-own is where costs can explode

Lease-to-own programs often appeal to shoppers who feel stuck. The pitch is simple. No credit needed. Fast approval. Low payment. Take it home today.

But the total cost can be shocking. Lease-to-own options often carry effective APRs exceeding 100% to 300%, and a $1,000 sofa can end up costing over $3,000, according to this financing comparison page. The same source says a 2025 CFPB report found that 40% of lease-to-own users regretted the decision because of unexpected fees and high total costs.

That’s a heavy price for “easy.”

If the monthly payment looks small, always ask for the full amount you’ll pay by the end. That number tells the real story.

A safer way to think

Use this quick checklist whenever a financing offer feels rushed or vague:

Ask for the total cost Not just the monthly payment. The total is what matters.

Read the deadline rules Promotions can be fine, but only if you understand the exact payoff window.

Watch for fee language Late fees, reinstatement fees, and processing charges can turn a manageable plan into a painful one.

Match the plan to the product A high-cost lease plan for a basic sofa often makes less sense than a transparent installment option on better-quality furniture.

If you’re trying to time a furniture purchase carefully, our thoughts on when is the best time to buy furniture can help you think through budget, urgency, and value together.

The BILTRITE Difference How We Make Financing Simple

A financing conversation feels different when it happens across a desk from someone you may see again at the grocery store, the school concert, or right back here in the showroom a few years from now. That kind of relationship changes how the process should work.

At BILTRITE, financing is part of helping you furnish your home well. It sits right alongside questions about comfort, room size, durability, and how long you want the furniture to serve your family. That matters because the right payment plan depends on what you are buying and why you are buying it. A mattress for better sleep, a lift chair for daily support, and a solid-wood dining set for the long haul do not always fit the same kind of financing approach.

Our team walks through those choices with you in plain language. If something is confusing, you can stop and ask. If one option looks affordable month to month but costs more over time, we can point that out. Good financing should work like a well-built table. Steady, clear, and built to hold up.

That personal guidance is what many shoppers miss with online checkouts. A website can approve or decline an application, but it cannot sit with you and sort out whether the plan fits your budget, your timeline, and the furniture you need. It also cannot learn your priorities the way a local salesperson can. One family may need the lowest payment that still feels safe. Another may want to pay faster and be done. Those are different conversations.

BILTRITE Furniture-Leather-Mattresses offers in-store financing conversations tied to the pieces you are considering in our Greenfield showroom. For many customers, the helpful part is not just filling out an application. It is being able to compare options face to face and ask the kinds of questions that do not fit neatly into an online form.

A good financing conversation should leave you feeling informed and comfortable enough to say yes, no, or not yet.

We are also a family business in the old-fashioned sense. We do not sell online, and we close on Sundays and Mondays so our families can be together. That keeps our focus where it belongs. On long-term trust, honest advice, and helping neighbors choose furniture and financing the right way.

Your Checklist for a Smooth In-Store Application

Most financing applications feel much easier when you come in prepared. You don’t need a briefcase full of paperwork. A little prep goes a long way.

Bring the basics

Have these items with you if you can:

A valid photo ID so the application details match your information

Proof of income such as recent pay information or another accepted income record

Basic contact information including your current address and phone number

A rough budget range so you know what monthly payment feels comfortable before you fall in love with a whole room

If you’re shopping with a spouse or partner and plan to apply together, bring what you need for both people. That can speed things up and make the decision process smoother.

Know your comfort zone before you shop

You do not need to know every finance term before visiting a showroom. But it helps to know a few simple things.

What item is the priority Sofa, mattress, dining set, lift chair, bedroom set

Whether you want short-term payoff or smaller monthly payments Those are not always the same thing

What monthly amount feels realistic Not “maybe we can make it work,” but what fits your budget

A quick credit check on your own can also help if you’re comfortable doing that. If your credit isn’t where you want it to be, don’t panic. It’s still useful to know where you stand before discussing options.

What to expect in store

Most of the time, the process is simple. You shop, narrow down your choices, talk through available payment routes, complete the application, and review the terms before agreeing to anything.

The big win is confidence. When you’ve brought your basics and thought through your budget, you can spend more energy on the enjoyable part. Trying the recliner, testing the mattress, opening the drawers, checking the wood finish, and seeing what works in your home.

Come On Down and Let Us Help You

You finally find the right sofa. The cushions feel good, the size fits your room, and you can already see movie night with the kids. Then the financing part starts to feel cloudy, and a purchase that should feel exciting suddenly feels heavy.

It does not have to go that way.

Good furniture financing should feel like a clear conversation, not a sales trap. You should know what you are agreeing to, what your payment will be, and whether the furniture still makes sense for your budget a few months from now. That is one reason many families still prefer working with a local store instead of clicking through a long online checkout or getting pulled into a costly lease-to-own offer that looks easy at first and gets expensive later.

At BILTRITE Furniture-Leather-Mattresses, we still do business the way my family was taught to do it. We answer questions plainly. We help you compare your options. We let you sit on the sofa, test the recliner, open the drawers, and make sure the piece is right for your home before you make a payment decision. That personal help matters, especially when financing is part of the purchase.

Our Greenfield showroom gives you something big online sellers cannot give. A real conversation with people who know furniture, know the financing process, and care whether you leave feeling comfortable with both. No pressure. No mystery. Just practical help from a local family business that has served Metro Milwaukee for generations.

If you have been waiting because the money side felt confusing, stop in and talk with us. We will help you sort through the choices, avoid the costly mistakes, and find a payment path that fits your home, your budget, and your family.

Come visit BILTRITE Furniture-Leather-Mattresses in Greenfield and talk with our family-friendly team about easy furniture financing, better-quality furniture, and mattress options that fit real Milwaukee homes. We’d love to say hello, show you our USA-made and Amish-made selections, and help you make a comfortable, confident choice for your family.